Double Disruption: Oil Shocks and AI Labour Revolution?

Investment Navigator, March 2026 Edition

Will Oil Price Shock Become a Reality?

We discuss the latest changes in our asset allocation views given the rising risk of a prolonged Iranian conflict that could keep oil and gas prices elevated for longer, and a more stagflationary economic scenario leads us to take a more prudent view on risk assets.

Bots vs Jobs. The Great AI Disruption Debate

For years, the idea that artificial intelligence (AI) could disrupt labour markets remained largely theoretical, a topic for futurists, economists, and policymakers. But in recent weeks, that narrative has moved from a simmering concern to action, driving cross-sector rotation, especially with the “sell software, buy semi-conductors” rotation.

The shift raises urgent questions: What triggered the cross-sector rotation? Is this a temporary market overreaction, or the beginning of a fundamental economic realignment? And if AI reshapes industries faster than expected, what does that mean for growth, employment, and corporate earnings?

Will Oil Price Shock Become a Reality?

Given the uncertainty over the Iran conflict remains very high, as reflected in the jump in implied volatility on oil, stocks and FX markets recently, we have decided to integrate the risk of a prolonged Iranian conflict into our asset allocation views. As the Strait of Hormuz is still constrained, we may enter the realm of oil demand destruction if the elevated oil and gas prices persist over the next few months, as was the case in 2022. Such a stagflationary economic scenario leads us to take a more prudent view on risk assets, notably both global equities, the high yield credit as well as emerging bond markets.

The risk of high oil prices for longer

The Brent crude oil price surged to above USD 100 per barrel on 9 March, up over 70% year-to-date. It is still highly uncertain when the conflict would end. With the effective closure of the Strait of Hormuz, combining with tanker traffic disruption and attacks on oil production and refining facilities, several Gulf states are temporary halting or reducing their oil and gas production. Thus, this supply disruption is real, and production could take longer than initially expected to return to pre-conflict levels. Even if President Trump blinks (due to pressure from markets and from Gulf state allies), will the Iranians allow the Strait of Hormuz to reopen to seaborne traffic?

Given the likeliness of ongoing supply disruption for longer, oil price spikes to USD 120 is still possible. Once there is some perspective on de-escalation, oil and gas prices could quickly pull back. But our initial scenario of Brent returning to its USD 60–70 trading range before year-end has become less realistic, as the original oversupply will now be absorbed by current temporary production outages. So, a more realistic 12-month target would be a range of USD 70–80.

Risk of a more stagflationary scenario

The economic consequences of higher oil prices depend not only on the magnitude of the increase but also on the price level and, especially, on the duration of the energy shock. A price level above USD 100 — and in particular above USD 120 — for more than two months would dramatically raise the probability of a stagflation and even a recession. Net energy importer regions such as Europe and Asia (such as Japan, Korea) are more vulnerable than the US and Latam (net oil exporters). China with significant oil reserves is also expected to fare better.

Tactically trimming risks to a more Neutral positioning, while preparing the shopping list

The risks of a prolonged conflict causing a more sustainable rise in energy prices have increased, and the risk-reward picture for risk assets has deteriorated. The situation might well become materially worse before it gets better. Hence, we tactically trimming some risks to a more neutral positioning in the short term. At the same time, investors should also prepare a potential buy list of opportunities to action IF the US do decide to “declare victory” and de-escalate the conflict, AND if ships begin to pass through the Strait of Hormuz once again.

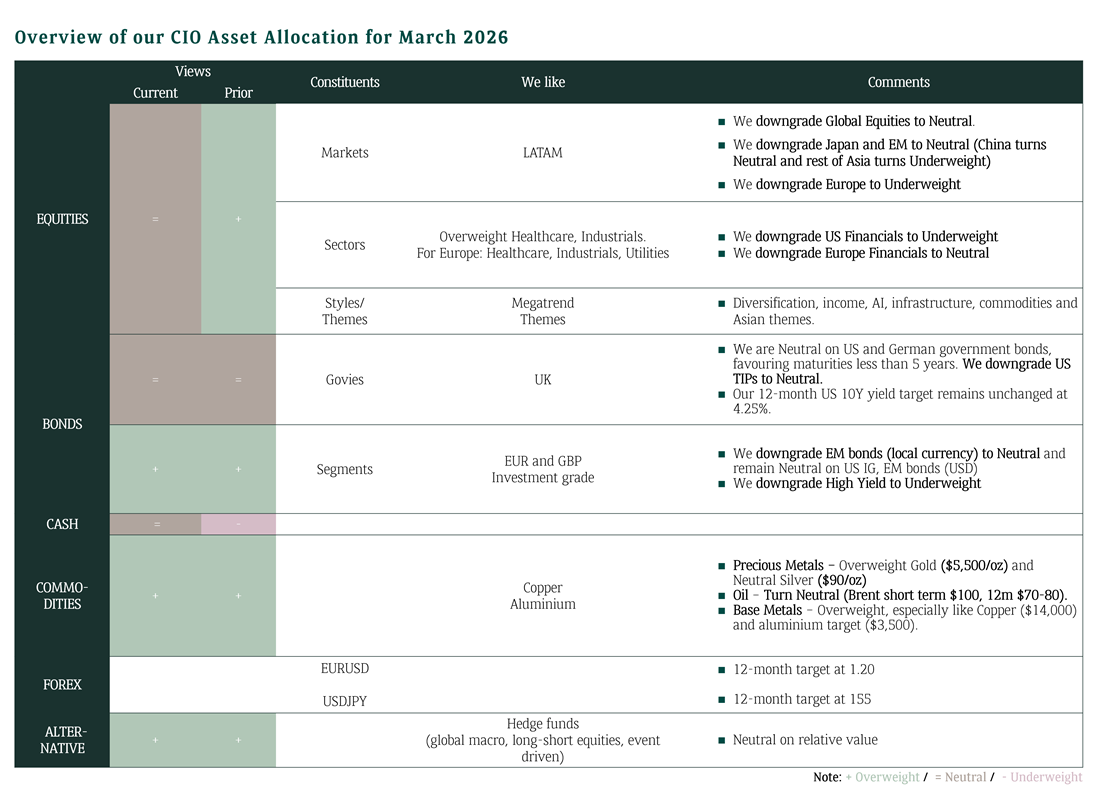

Summary of our changes in asset allocation views

Fixed Income

- Downgrade High Yield to Underweight

- Downgrade EM local currency bonds to Neutral

Equities

- Downgrade Overall Equities to Neutral

- Downgrade Japan to Neutral

- Downgrade EM to Neutral (Downgrade Asia to Underweight with China turning neutral and rest of Asia Underweight; Keep Latam OW)

- Downgrade Europe to Underweight

- Downgrade US Financials to Underweight and Europe Financials to Neutral

Forex

- Expect USD to strengthen in the short term, and less USD downside in the medium term

- EURUSD 3-month target 1.14 (from 1.18), 12m target 1.2 (from 1.24)

Bots vs Jobs. The Great AI Disruption Debate

The catalyst: A viral narrative

The sector rotation was not triggered by a broad earnings miss or a hawkish central bank pivot, but rather by a viral blog post on X. The piece, authored by independent researcher Citrini and titled “The 2028 Global Intelligence Crisis," quickly amassed millions of views, hardly surprising given its timely subject matter and the fact that it is both well-written and thought-provoking.

Despite the authors explicitly stating at the outset that the post is not a prediction but rather an exploration of an underexamined scenario, it appears to have been received as something it was never intended to be—namely, in the authors’ own words, "AI doomer fan-fiction.”

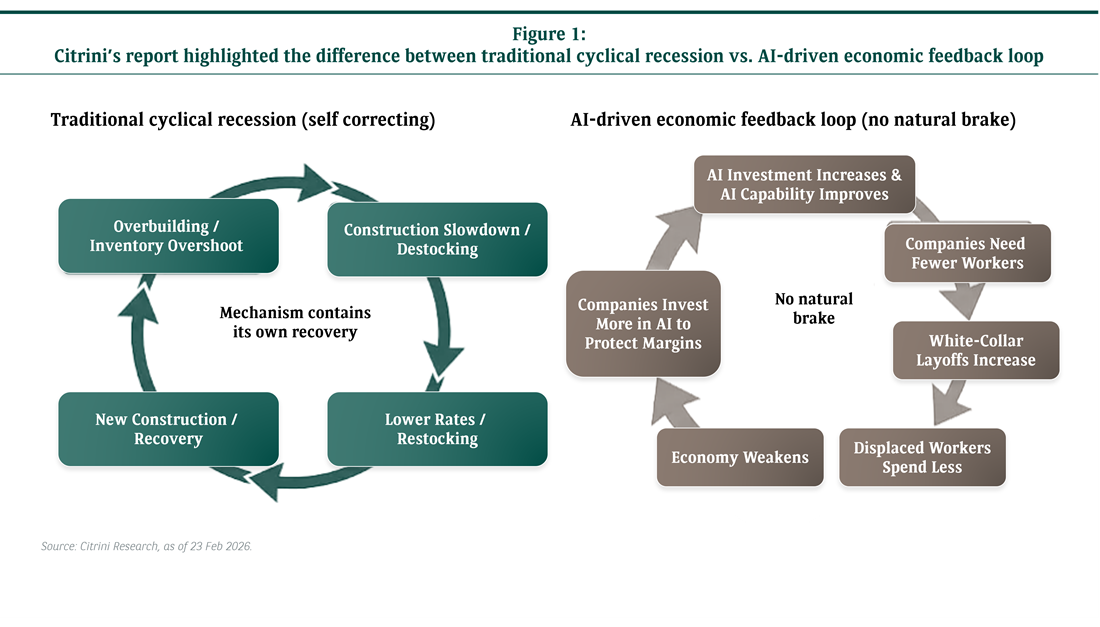

At its core, the scenario outlines a future in which AI disrupts the vast majority of white-collar service jobs, as companies increasingly adopt AI to cut costs (and ensure survival), rendering more workers redundant. With declining incomes, the consumer economy weakens, prompting further cost-cutting through AI—which, in turn, displaces even more workers. The result is a self-reinforcing negative feedback loop.

Let's separate signal from noise...

Fears of an AI-driven economic collapse assume an unlikely sequence of events: extremely rapid labour displacement, minimal reinvestment of corporate profits, no meaningful policy response, and unconstrained technological scaling. Economic history suggests this combination is improbable. Previous general-purpose technologies, from electricity to computing, raised productivity and ultimately created new industries, new forms of demand, and new employment.

Artificial intelligence is therefore more likely to act as a productivity amplifier, rather than a macroeconomic destabiliser. In a world facing demographic aging, supply-chain fragmentation, and rising fiscal pressures, AI could instead help sustain trend growth. Industries will be disrupted and the speed of diffusion will be key. The real uncertainty is not whether AI will generate economic value, but how that value is distributed across labour, capital, and institutions.

Which sectors are AI benefiting, and which are AI disrupting?

Artificial Intelligence is transitioning from a research breakthrough to a broad economic platform comparable to the advent of the internet or the industrial revolution’s adoption of electricity in the past. Generative AI alone is estimated to add $2.6–4.4 trillion annually to global GDP through productivity gains across industries. Meanwhile, up to 300 million jobs globally could be partially automated by AI technologies over time. For equity investors, this shift is already creating clear winners and potential structural losers. That said, it is likely that displacement won’t be that swift, but how to parse these conflicting signals?

Sector Winners

1. Semiconductors & Compute Infrastructure

AI models require massive computational power. Training large models can require tens of thousands of GPUs, driving demand for advanced chips and networking.

Key beneficiaries:

- The whole value chain from semiconductor capital equipment to semiconductor companies

(the global AI semiconductor market is projected to exceed $400 billion by 2030, growing at over 25% CAGR) - Data center networking

- Memory manufacturers (HBM)

- Power and cooling infrastructure

This sector represents the “picks and shovels” of the AI boom. However, keep in mind the sector is cyclical and the length of the capex boom is key. The ROI on AI will also be the key determinant of the length of the cycle.

2. Cloud Platforms & Hyperscalers

AI deployment requires large-scale compute infrastructure and model hosting. Major platforms, such as the hyperscalers, are embedding AI into cloud services and enterprise software.

These companies are also benefiting from:

- recurring AI infrastructure revenue

- software productivity tools

- enterprise AI platform ecosystems

Cloud AI spending is expected to grow from roughly $50–60 billion in 2023 to over $300 billion by 2030. Enterprise customers are increasingly integrating AI copilots, automated coding tools, and customer-service models directly into workflows. However, competition among hyperscalers is also picking up and they will likely generate less free cash flow and will have lower buybacks going forward if capex remains elevated (rising capital intensity). Hence, stock picking will be crucial.

3. Software Automation & Productivity

AI is disrupting knowledge work by automating coding, marketing, legal drafting, and analytics. Software companies incorporating AI into productivity platforms can expand margins while increasing product value. The key will be first movers in software space that incorporate agents and have proprietary data that will not be commoditised by AI in general. This sector will be disrupted but rising stock dispersion means stock selection can generate alpha.

Examples include:

- coding copilots

- automated customer support

- AI marketing and design tools

4. Robotics & Physical Automation

AI is moving from digital automation into physical environments such as warehouses, logistics, and manufacturing.

Advances in machine vision and reinforcement learning are enabling:

- warehouse robotics

- autonomous delivery

- industrial automation

This creates long-term demand for robotics hardware, sensors, and automation software.

Possible sectors disrupted

1. Business Process Outsourcing (BPO)

Customer service, call centers, and data processing are among the most automatable tasks.

Generative AI chatbots can now handle 60–80% of customer queries, potentially reducing demand for large offshore service providers. Countries heavily reliant on outsourcing labour may face employment disruptions.

2. Entry-level Knowledge Work

AI can automate tasks such as:

- legal research

- basic financial analysis

- marketing content generation

- software debugging

This may compress margins for professional services firms and reduce demand for junior roles.

3. Legacy Software Vendors

Companies relying on traditional SaaS models without AI integration risk disruption. AI-native platforms could replace expensive enterprise tools by providing more automated workflows and decision-making. The winners will be the ones having proprietary data and agentic AI integration.

Please read carefully the disclaimer: https://bnpp.lk/-asia-disclaimer